In the throes of a full COVID-19 pandemic, most business leaders’ top priority is rightfully the health and safety of their employees, families, and communities. Even though business disruptions are significant and overwhelming, the primary efforts focused on both safety and the control of the spread of SARS-CoV-2, like social distancing and working remotely, are paramount.

Without diminishing the importance of those priorities, business leaders also need to think about the viability of their organizations and rapidly embrace strategic planning around the crisis. For biotech leaders, this involves strengthening efforts aimed at mitigating the negative consequences of the pandemic on the advancement of the industry’s pipeline of new medicines. Before addressing those issues, it’s important to put the economic changes and biotech’s unique capital market dependency in context.

The COVID-19 pandemic crisis has created panic in the markets: the fear index has hit its all time high, as volatility and uncertainty about the future skyrocket. Incredible gyrations in the stock market happen every few days, in both directions. Huge dislocations in the economy are happening due to the pandemic, both from the virus itself and from our efforts to “flatten the curve” around shutdowns, social distancing, and remote working. This impacts are not only with hospitality and T&E businesses (like Marriott’s 90% revenue drop in a few weeks), but also with housing (mortgage applications off significantly), energy, education, consumer goods, restaurants, and nearly every other sector.

Morgan Stanley and Goldman Sachs economists are now estimating -30% and -24% drops in the quarterly GDP in 2Q2020, more than double the largest drops in history (from the start of the Great Depression). Unemployment claims spiked and will almost certainly continue going up, bringing the US unemployment rate to 12.8%, a rate not seen in decades, according to Morgan Stanley. A massive stimulus program is coming together to supposedly cure the economy of the coronavirus pandemic. However, there’s significant uncertainty around what the post-pandemic world will look like. Will we see a rosy “V-shaped” or optimistic “U-shaped” recovery of the overall economy, or will it be a more challenging “L-shaped” slog.

But what about the biotech sector?

Biopharma stocks have weathered the storm better than many sectors, likely due to the industry’s role in the possible COVID-19 response, as well as focus on making new medicines in general; new therapies are largely “recession-proof” if they address real medical needs. The two key biotech indices, the market-weighted NASDAQ Biotech Index ($NBI) and the equal-weighted S&P Biotech Index ($XBI) are off 16% and 25%, respectively, since peaking in mid-February. For comparison, we’ve seen much more significant “corrections” during two periods in the recent past: during 2H 2015-1Q 2016, the XBI was off 48%; in 4Q 2018, it was off 35%. This pandemic panic has lots of room to run so the markets could correct to those levels (35-50%), but I think that’s unlikely.

R&D-stage biotech firms, represented by the vast majority of private and small/mid-cap (SMid) public companies, are loss-making enterprises. They don’t have product revenues in most cases, so this pandemic won’t be affecting their sales. Consumers and their health plans don’t buy R&D-stage drugs, so changes in consumer behavior aren’t relevant in the near-term. Loss-making biotechs largely don’t have much debt financing, so tightening access to credit is not a major factor in our space.

But these emerging biotechs do have to raise funding, largely from the equity markets, to advance their R&D portfolios. In the absence of revenue multiples or other conventional financial metrics, for these loss-making biotechs, data is the ultimate currency of progress and market value. Data comes in lots of flavors: large Phase 3 outcomes, human “proof of concept” Phase 2 clinical results, safety and tolerability insights from Phase 1 studies, and preclinical experiments, among many other flavors. Fundamentally, R&D progress is measured by these data and their attractiveness; future accessibility to additional funding is often very tightly linked to favorable and advancing R&D-stage data packages.

This is where this COVID-19 crisis directly impacts biotech: the ability to get key value-creating data will affect the ability to get future funding; and, without cash, biotechs can’t get to those key data. Importantly, even with great execution and delivery to timelines, most companies will encounter a higher cost of capital for their next financing if current conditions in the equity markets persist. Those without data in hand will likely face real challenges.

For C-level executives and Boards of biotech companies, it all comes down to an assessment of how current cash positions link to the operational burn rates required to get to the key data inflections. It’s critical to think through how to get to data in an uncertain macro environment, and thus uncertain equity capital market, in a panic-stricken world with significant execution challenges.

R&D execution challenges

This COVID-19 pandemic is likely still in its early innings, so how prolonged the impact on biopharma business operations will last is uncertain. But one thing is very clear: the dislocations across the global economy will almost certainly create delays in our R&D timelines, as has been described in regular columns by Adam Feuerstein at STAT News. Here are some further examples across the R&D value chain.

Clinical development programs are particularly sensitive to the COVID disruptions. With the shutdown of the healthcare system in multiple regions of the world, and hospitals in particular, the impact on clinical trial timelines has the potential to be significant. Many sites have prohibited all elective procedures, which includes non-urgent visits and treatments for most non-life-threatening diseases. Patient screening and enrollment may be shutdown or curtailed dramatically in some geographies/sites due to travel and logistics restrictions. IRB’s at medical centers aren’t meeting to review new trial applications or approve protocol amendments. Site initiation visits are going virtual, if they are happening at all. Potential safety issues (or confounding issues) around using immune-modulating experimental agents during an infectious pandemic are now real considerations. Logistically complex trials, like those in cell therapy, are particularly difficult in this environment. All of these pose big challenges to small biotechs that were expecting to enroll patients over the next few quarters in order to obtain the key data to catalyze a future financing. But small biotechs aren’t the only ones facing this issue: Lilly recently announced delaying new trial starts and pausing enrollment in existing studies, and BMS is halting new enrollment in cell therapy studies.

Drug discovery and preclinical activities are also being pressured. Timelines in early R&D can be greatly affected by availability of key animal experiments (like IND-enabling GLP studies or critical pharmacology models) and manufacturing activities. The pandemic has created real concern around the availability of both CRO partners and vivarium access to be able to conduct these studies. When the crisis was initially hitting China in January, many feared that Chinese CRO partners there would be out for months and wreak havoc on R&D timelines; that situation has now changed. It’s the CROs in the US and Europe where the big worries are, and China appears to be coming back online. In fact, some of our discovery-stage companies have increased their efforts in China in the past week or so. For biotechs with wet labs and in-house scientists, social distancing has certainly made productivity challenging. To protect employees, a number of larger biopharma companies have moved to “red team/blue team” models to create space and safety precautions while continuing lab operations. Fortunately, in Massachusetts, biotech R&D scientists are considered essential and exempt from “cease business operations” and “work from home” orders announced by Gov Baker. Further, for both office and lab team members, there remain significant unanswered questions around how and when to re-engage back in the workplace (e.g., what are the local or national pandemic metrics we’d need to see to ramp back up). These scientific business disruptions are undoubtedly going to affect many companies’ early stage R&D timelines.

Academic partners are critical collaborators for many early stage biotechs, and they are similarly facing productivity challenges. David Sabatini of MIT’s Whitehead Institute summed it up best via Twitter: “I’m pretty tired of hearing how we scientists are supposed to be so productive now. Anyone with kids, elderly parents, lab members to worry about, stranded masters students, etc is too stressed and busy to be thinking big thoughts.” This is a sentiment shared by academic and industry scientists alike.

Lastly, many other areas of a biotech’s business operations are also challenging. Logistics around CMC processes, ordering supplies, shipping drug substance, moving experimental reagents to other partners, etc… Space issues, never easy in challenging real estate markets like the Boston area, are also now fraught with COVID-induced complexity: building permits aren’t being acted on in many geographies, construction crews can’t engage on new lab/office space, delays to moving in mean delays to key lab equipment, leaving existing space will be hard for tenants without new space, etc… If a biotech planned to move into new space this fall after a summer buildout, those plans are likely going to be delayed – with ripple effects on R&D and organizational growth/constraints.

All of these potential sources of delay can impact the one critically important goal: getting to key catalytic data that demonstrates the value of an R&D program or portfolio.

Management teams should be doing everything in their control to optimize the execution parameters and mitigate the downside impacts on project gantt charts and timelines. Now is the time to consider “insurance” on your operating plans – adding a new clinical site or partner that can carry the execution while certain parts of the globe are offline. Putting in place the right executional “hedge” for protection of your timelines requires thinking through tradeoffs and don’t come for free. A big part of this strategic planning process involves understanding the bookends of uncertainty and the levers we can control.

Scenario planning

The macro environment and the dislocations in the economy are not things we can control as biotech executives; the key is to understand the range of possible outcomes, handicap their likelihood, and prepare accordingly. There are likely short, medium, and long term macro scenarios for the impact the COVID pandemic will have on biotech R&D.

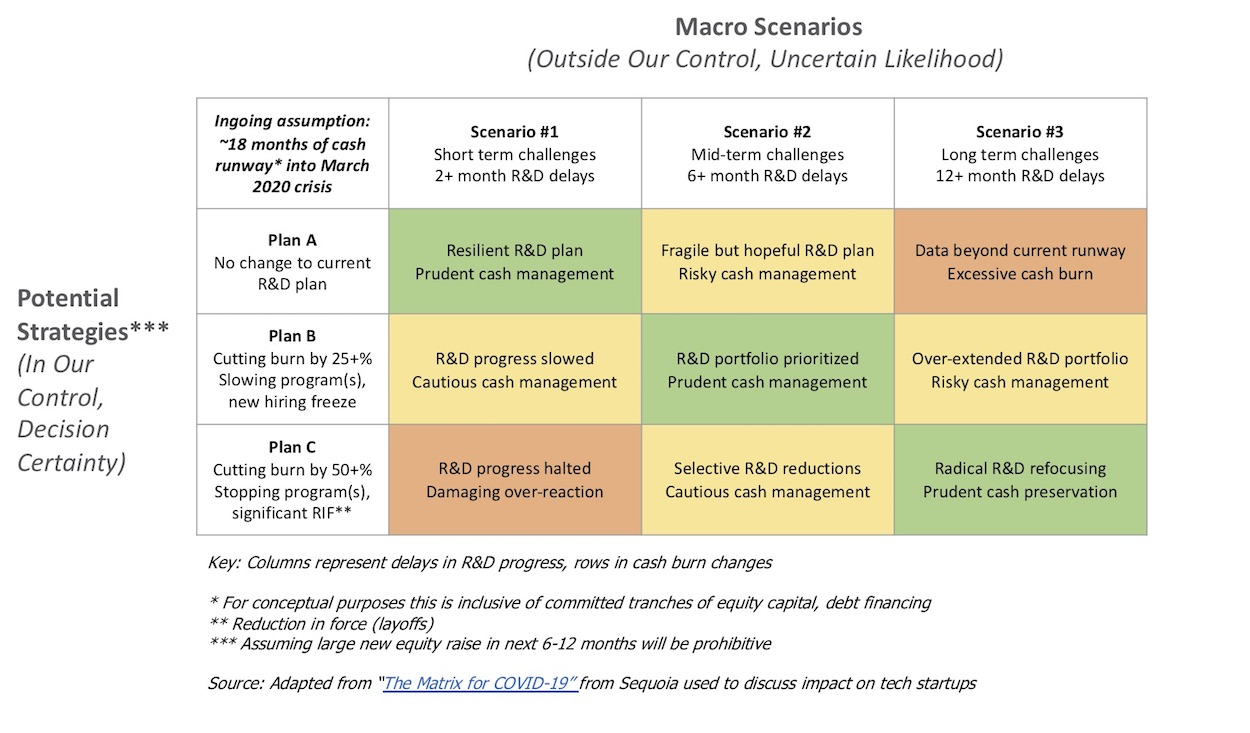

As described in the matrix below (adapted for biotech from Sequoia), there’s a rosy if not overly optimistic scenario that the practical R&D delays are minimal (Scenario #1), where they may be limited to a few months. We often plan for a few months of delays in the normal course of business in R&D (timelines, amazingly, often slip out by a quarter). Scenario #1 is likely just a pleasant daydream at this point. The middle scenario (#2), and probably the most likely in my opinion, is that there are real delays that continue to impact us through the fall (“medium term”), with key R&D timelines moving out by six or more months. The pessimistic scenario (#3) is that we face long term consequences of this pandemic on R&D timelines, leading to significant delays that add a year or more to program timelines. For the purpose of discussing the strategic planning implications, a working assumption is that the structural delays arising in these scenarios are only capable of being mitigated at the margin by operational excellence, contingency planning, backup vendor management, and the like. These are macro factors largely out of our control.

Assuming a typical loss-making R&D-stage biotech found itself entering March 2020 with roughly 18 months of cash, how should one respond to these three macro scenarios? If the equity capital markets are closed or prohibitively expensive for raising significant additional funding, then there are several potential strategies to embark on.

If you feel strongly we’re in Scenario #1, then not fundamentally changing your R&D efforts (Plan A) may actually be the smartest long term decision: you have the cash to get you through the key data inflection points, and will be able to raise in 2021 after the pandemic and election are behind us. But under other macro scenarios, especially #3, doing nothing runs real risk of an impossible cash burn and runway situation: you’ll never get to the data you need to create value. This is the domain of recapitalizations and liquidations.

In Plan B, management teams exhibit more caution on their spending – aiming to cut burn (extend runway) to ensure that in the middle macro scenario of six month delays, you can still get to data with breathing room on the other side. In Plan C, fear takes over – and is essentially smart only if you are preparing for a “nuclear winter” with macro scenario #3. In any more modest macro setting, Plan C is an over-reaction and damages the organizational culture and its R&D prospects.

This is a Goldilocks moment for strategic planning: not too hot and not too cold. Prudent cash management that funds a biotech to the key data is the objective. Too optimistic and you risk driving off a cliff; too draconian on the cuts, and you hurt your longer term prospects.

This conclusion seems clear in the abstract for the “typical” biotech. But no biotech is typical – there are nuances around the R&D program(s), time to data, cash positions, burn rates etc… Which scenario plan (A, B, or C) makes sense for a given biotech depends on lots of company-intrinsic factors – hence the challenge to management teams and Boards.

But it’s important for biotech executives to go through a strategic dialogue with their Boards, framed by a matrix like this, and talk through the specifics of their situation and how different macro scenarios can impact their company.

Near term optionality

In the face of these macro uncertainties, buying some time – optionality – in the near term seems like the smart leadership. We’ll know better over the next couple of months whether we’re trending to macro scenarios #1-#2-#3. Right now biotechs should work to preserve strategic optionality around their path to data and future capital raises.

In the near-term, this means most biotechs should be working off a new 2020 “interim” base case operating plans that incorporate the possible macro downsides, where all key data points (e.g., development nominations, IND’s, PoC’s, Phase 3’s) could be delayed by various degrees.

Being short of key data readouts and running out of cash is a challenging place in any market, but will be particularly challenging in the near term. Companies needing to tap the equity capital markets for financing over the next 3-4 quarters could find it incredibly costly, and the cost of capital is only likely to worsen considerably if we are in the mid- to long-term macro downside scenarios.

Over the next couple months, here are five no-brainer decisions to act on in the near term:

- Focus on optimizing your virtual execution model.With social distancing likely to persist (to varying extents) in the months ahead, biotechs need to step up their game on remote operational excellence. This includes working closely with global partners to create new SOPs for how to engage on virtual project teams. Investing in new working models will help. Sharing of best practices by executive teams across the industry is happening organically, and these should have positive impact. This is the only way timelines don’t take a massive hit. This is where core corporate values come into place, as has been described by Surface and Synlogic executives in recent blogs.

- Conserve capital in the near term.To buy some optionality, reprioritizing resources to the key program(s) and pressing pause elsewhere for a couple months makes sense. This may mean slowing down non-essential hiring in the near term (e.g., a “hiring freeze”) and minimizing non-critical capital expenditures this spring. If your lab isn’t operational, perhaps delaying the planned lab hires or equipment. Unless you are certain about the magnitude of your expected delays and or macro view, doing painful reductions in force (RIFs) right now would be premature. Things may change as visibility gets better this spring, but right now buying strategic optionality is important. In a few months, significantly cutting burn, or ancillary programs, to ensure the viability of the lead program(s) may be prudent management but more visibility is needed.

- Shore up your balance sheet. The cost of capital is likely to go up over the next few months, so lock in any closings of equity capital in the near term. Rounds are still getting done as planned: we’ve had or will have a dozen financings close in March-April this year, and co-investors have all stepped up despite the turmoil. Teams should also consider whether venture debt or credit lines can help them get through data windows. Raising money in the summer if the macro scenarios shift towards #3 could be very challenging for loss-making biotech companies. Also worth considering if SBIR and other non-dilutive sources of funding make sense, as those are long lead time items. In addition, the details of the current pandemic stimulus plan aren’t clear, but this could involve financial support for the sector if 2009 is any guide, where $10B was earmarked for biomedical research.

- Seek Pharma partners openly and actively.The reality is Pharma has cash flow and huge warchests, which is likely going to continue even in this pandemic crisis. Beyond just cash, Pharma can bring stability to programs and reduce the entropy associated with operating in a pandemic. Finding good long-term partners could be especially valuable for platform companies with broader portfolios; since the equity markets may be less accommodating, pharma partners may help advance non-lead programs. Regional deals for China or Asian rights may be worth pursuing as a way to strengthen balance sheets. Option deals, recently out of vogue, may be of interest again to hedge future uncertainty. 2020 is likely the time to get good deals done, and to not let the perfect deal be the enemy of the good. I’d expect to see partnering announcements pick up in the latter half of the year.

- Remember Eisenhower: “Plans are worthless, but planning is everything”. Right now we are surrounded by uncertainty and volatility, so it’s far more challenging than “normal” to fix a strategy in stone. Continually revisiting our assumptions as we learn more in this unfolding pandemic is critical for modifying our strategic and operating plans: adaptability will be the hallmark of winning companies. It’s critical to think through the various contingencies if Scenario #1, #2, or #3 – or another variant of them – emerges. In addition, it’s valuable to understand how fundraising windows play into the “degrees of freedom” you have for decision-making; wait too long for certain decisions and you may lose the optionality, or vice versa – some choices are mutually exclusive with others. All this comes out in thorough planning process. Engage your Board and your key shareholders in your various battle scenarios.

During a once-in-a-decade crisis like COVID-19, biotech executives need to step up their strategic game and integrate various macro scenarios into their planning. We won’t have great visibility for a few months on how the COVID pandemic disruption will play out for biotech’s R&D programs, but buying optionality in the near-term and pushing a candid assessment of strategic plans is critical.

Hopefully, with the right strategic discussions and decision-making in the near term, the biotech sector can avoid being paralyzed by this market dislocation and collectively advance our innovative R&D pipeline through to their next inflection points. Patients need these new medicines regardless of a viral pandemic.