Today we announced the closing of Atlas Venture Fund XI, a $350M investment vehicle focused exclusively on early stage biotech investing.

Since launching our fundraising process in April, we’ve received a truly humbling level of support and interest in our strategy from new and existing Limited Partners, and closed the fund heavily oversubscribed above its original target. A successful fundraise depends in large part on the entrepreneurs who have not only delivered great outcomes but also provided their positive “war story” references on their VCs in the process – so thanks to all of the great entrepreneurs (and co-investors) we’ve had the privilege to work with!

With the closing of Fund XI, we’re focused on continuing to deliver on our mission: doing well by doing good. Advancing transformative therapies for patients is incredibly motivating – it’s the exciting purpose that gets us all out of bed in the morning. And, over the long term, there’s a tight correlation in the biopharma sector between having real impact on patients’ lives and generating attractive investment returns. It’s the essence of our mission.

Our fundraise was the fastest and most oversubscribed effort we’ve had in over 15 years, and it’s our third vehicle since 2012, marking a 2.5 year average cycle time. Solid returns are of course a big driver of this, but so is a coherent strategy for continuing to generate them in the future. Our approach has taken advantage of the congruence of at least five bullish macro tailwinds over the past few years:

- massive unmet medical needs, only accelerating with the “greying” of society, exist around the causes of both morbidity and mortality, placing a premium on real therapeutic innovation as one of the most efficient forms of healthcare delivery;

- continued and increasing externalization of research by large biopharma companies, with therapeutic discovery now distributed across the ecosystem rather than inside of monolithic R&D groups;

- constrained “supply” of new, high quality biotech startups, due to the scarcity triad of talent, resource, and substrate inputs, in the face of significant downstream demand – creating a favorable supply/demand imbalance;

- further “virtuous cycle” consolidation of resources and talent into Boston as a premier global translational center for biomedical advances; and,

- cooperative global regulatory environments have emerged to facilitate the development and market entry of transformative therapies, while encouraging innovation-spurring competition

These five positive drivers remain in place today, and likely will continue for the foreseeable future – reinforcing the productive environment for our early stage strategy. Against this backdrop, it’s worth emphasizing some of the key themes underpinning the Atlas model.

We are tightly focused on seed-led biotech venture creation. This strategy has four important operational elements – discover, derisk, shape, and strengthen: that is, discover high impact science around which we create new startups; derisk this science early via our seed approach of validating the foundational premises with minimal capital, often incubating these young startups in our offices; shape the biotech business model to the opportunity (e.g., product engine platforms vs asset-centric plays); and strengthen by bringing the best of the firm, our broader network, and ecosystem to bear as we move from through the process of “prove-build-scale” for our startups. Via this model, we’ve helped co-found an average of six seed-stage biotech companies per year for the past few fund cycles.

We embrace scientific risk at Atlas – it’s the essence of what we do. In many ways, it’s just back to the basics: high risk, high return. By going early stage, we throw ourselves at cracking science risk, whether it be new biological mechanisms, new modalities, new translational approaches. By definition, this makes us a science-first investment firm. We’ve demonstrated we can titrate capital into these early stories and have the discipline to walk away when the science doesn’t play through favorably, leading to very attractive dollar-weighted loss ratios. We avoid the conventional late stage product risks (e.g., regulatory, commercial, reimbursement risks), not to mention idiosyncratic Phase 3 event risk, by staying focused on early stage R&D. We do this by participating early in the bench-to-bedside translation process, derisking the story, and finding the right downstream partners to help address those potentially big ticket later stage issues (either Pharma or the public markets) that are hard to fund via venture diets. High innovation quotient startups are the key to driving this early interest from downstream partners.

Our startup portfolio is, as you might expect given this strategy, chock full of cutting-edge science. I recall a few years ago when a Pharma R&D head, after reviewing our portfolio with us during the JPM conference, said “Congratulations on having such a high risk portfolio” – at the time I wasn’t quite sure how to react. But it’s our high risk portfolio – Nimbus, Padlock, Delinia, Intellia, Arteaus, CoStim, Stromedix, Avila, and many others – that has delivered handsomely on the second part of the risk/return equation. And our emerging portfolio is more of the same when it comes to embracing risk: engineered cell therapies (T-cells and bacteria), HSC transplant modalities (including ex vivo lentivirus gene therapy), oncolytic viruses, novel neuroscience, and various exciting new versions of drugging-the-undruggable, to name a few.

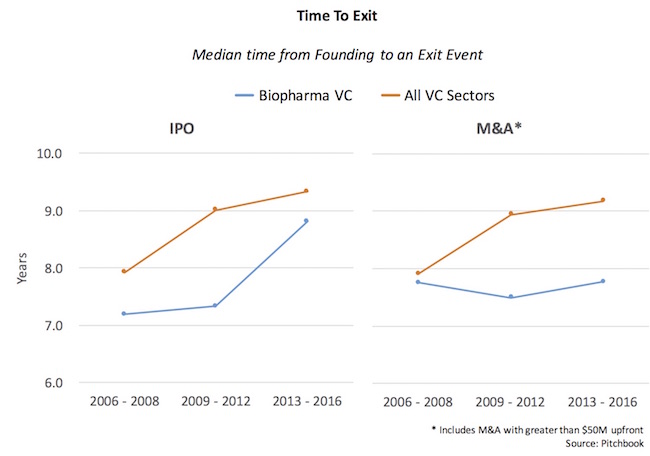

We also celebrate, and work to catalyze, the duration paradox of early stage investing. From an investment model perspective, holding periods are crucial variables in determining returns, and a largely unappreciated aspect of early stage biotech investing is that it can have remarkably short holding periods. Conventional dogma is that early stage takes too long, costs too much – because it takes 10-15 years to make a drug (as if getting a drug approved was the only trigger for investment success). This “takes too long” bias, which I’ve opined on before, just hasn’t been borne out in the past few fund cycles for Atlas, nor across the sector. Transformational therapies often reveal their potential early, and, even recognizing the later stage attrition risks, are often able to attract early partners or public market interest. Delinia was acquired less than 15 months from our seed investment (here); Intellia went public two years from founding (here). The median time to event for our last eighteen M&A exits and IPOs is only 5 years, and it’s less than 3 years for the nine M&A exits since 2013. Early stage paradoxically doesn’t imply longer holding periods – if one focuses on high demand, innovative new medicines.

{kind=link}

We value and invest deeply in cultivating meaningful relationships across the broader biopharma ecosystem. Tight linkages among the critical stakeholders in the biopharma universe are essential for our model, like most early stage biotech strategies. Looking upstream, we source the majority of our scientific substrate from academic labs all over the globe: about a third of our startups have connections in Boston, another third around the rest of the US, and the remaining third from Europe and Asia. Science competes globally, so our “idea discovery” catchment area needs to cover many of the great academic centers around the world. Turning downstream, we spend considerable energy focused on building and maintaining deep connections with both larger biopharma players and the public capital market buyside. These relationships are critical – both for accessing the necessary development-stage capital required to bring medicines to patients, but also for the shared information flow. Accessing deep expertise that exists in “the best of Pharma”, and with the thought-leader buyside asset managers, can be very helpful in advancing the next generation of great startups.

In addition to a broad range of more general relationships, we also have larger pharma companies as LPs, or Corporate Strategic Partners (CSPs), as we did in our prior two funds in 2013 and 2015. With Fund XI, Novartis has returned for its third fund as a CSP – we’ve successfully worked together on a number of investments and partnerships over the past few years (e.g., CoStim, Surface, Intellia, Luc, among others). In addition, we’re excited to announce that Takeda has joined us as a new CSP and we look forward to working with them. This relationship is one of many outreach efforts that integrate into Takeda’s ongoing R&D transformation and its embrace of the external innovation ecosystem. Lastly, Amgen remains a CSP in our prior vintage funds, and we maintain close ties to their R&D team. Importantly, as emphasized in the past, these CSP relationships are truly “open market” – they derive value through both strategic proximity and bidirectional active engagement, but do not constrain our portfolio companies or investment strategy in any way.

Beyond academics, pharma, and the buyside, we’ve also built deep and important relationships in the entrepreneurial community. Entrepreneurs-in-Residence (EIRs) are key to our model of in-house company creation, and continuing to expand their ranks over time is essential as they move into full-time roles in maturing startups. Further, as our venture creation model has grown over the past few funds, serial EIRs that cycle through multiple startups in the Atlas family are not only increasingly common but also hugely valuable – as they are able to share their startup learnings, and cultural imprinting, with newer EIR team members. Maintaining a vibrant startup community focused on great people is a significant focus of our team – as people matter more than anything else in this business.

Two final points to note.

We take a long view of the future of our firm and our team. Succession planning is one of the biggest modes of failure in venture and private equity partnerships, often due to a divergence in economics and governance rights between different generations of partners. Beyond its deep cultural ramifications on how we operate, our flat and equal partnership structure solves for this succession challenge. We recently announced Kevin Bitterman’s addition as a partner at the firm, and are thrilled to have him on board. As we start investing out of Fund XI this fall, Peter Barrett will transition into a venture partner role where he will focus on actively managing existing Atlas investments and assisting in firm-level operations. Importantly, Peter will remain a core and active member of the Atlas team, and isn’t retiring anytime soon – but he’s facilitating the kind of thoughtful succession planning that makes for stable, sustainable, and successful partnerships over the long run.

Lastly, we’re thrilled to be working on behalf of a great group of LP’s who share our mission of doing well by doing good. Venture capital funds are long duration investment vehicles, often exceeding 12-15 years. Once LP’s commit, they are essentially locked into a decade of “capital calls” (funding contributions). Unlike mutual funds and most hedge funds, where investors/LPs can withdraw their capital quickly, LPs in venture firms are committed to the long haul. This makes the relationship between the investing partners (GPs) and LPs so important – since we’ll likely be working together for at least a decade and sometimes several. We were fortunate in raising Fund XI to have demand far in excess of our fund size, which we capped at $350M to maintain the discipline around our seed-led venture creation model. This allowed us to selectively bring together an LP base that shares our patient-centric mission. Of course we want (and plan) to generate a great financial return for our LPs, but we also like to know that they are putting their assets to work on purposeful, meaningful endeavors that can better the world. Almost every one of our Fund X LP’s have come back to join us in Fund XI, and we’ve added more than 25 new LP’s in the fund that fit this profile: we now have nine university endowments, five charities and religious foundations, four museums, three hospitals, a number of pension and insurance plans, and a host of philanthropic family offices dedicated to a range of important causes. These are great people, great organizations, and great causes – and it’s truly a privilege to be working on their behalf.

To all of those who have supported us in our journey at Atlas, thank you. Looking forward to working with you and the rest of the ecosystem for years to come on the next generation of transformative new startups and their potential medicines.