A couple years ago we unveiled a new startup called Nimbus Discovery LLC which was experimenting with a new model that combined three key elements: Schrodinger’s cutting edge in silico drug screening and design platform, a truly virtual and globally distributed operating model for drug discovery, and an asset-centric LLC-based corporate structure (discussed here).

Although it’s too early to tell what eventual value will be created from this experiment, the company’s early biomarkers are strongly positive. Nimbus has cracked two very tough-to-drug targets of high interest to Pharma (immunokinase IRAK4 and lipid-pathway regulator ACC), and is entering IND-enabling development this year. The technology and virtual operating model have worked well together in efficiently delivering high quality drug candidates.

Importantly, the market validation of the model has also been positive: today Nimbus announced a deal with Monsanto, and last month announced a similar deal with Shire – both involve collaborative drug discovery with a pre-defined path to liquidity around those projects. Given the unique nature of the deals, I thought it would be worth sharing more details and a few general reflections on the model.

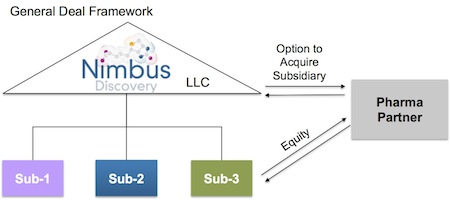

Both deals are structured to take advantage of the Nimbus asset-centric approach: they involve equity or equity-like investments in individual R&D programs housed in standalone subsidiaries, alongside an option to acquire those subsidiaries at a specific milestone with pre-negotiated deal economics. These are very enabling for Nimbus: project-based resourcing to support the prosecution of a pipeline with clear value creation points defined at the outset without the need for dilutive funding at the parent LLC level.

These collaborative deals were born out of close relationships Atlas has with both Monsanto and Shire. Over the past few years, both companies have been able to watch Nimbus deliver against its existing programs, in particular for ACC, IRAK4, Tyk2. Here’s the short promotional on their programs’ progress On ACC, it took Nimbus only 16 months from standing start with a virtual screen to get to a fully characterized Development Candidate (DC) with a first-in-class allosteric regulator of the target; for IRAK4, the team has discovered truly selective inhibitors with potent in vivo activity and DC-like profiles; and lastly, they have cracked the Tyk2 selectivity challenge vs closely homologous JAK2 and other JAK family members. The progress of these case studies and the familiarity they had with our team definitely facilitated both transactions. More evidence for why tighter collaborative Pharma/Venture relationships are value-creating.

The bigger picture: why these deal structures make sense

- For the biotech, these deals help build a portfolio comprising multiple program-focused entities under an LLC umbrella. In some respects, the pipeline becomes a collection of call optionson individual paths of potential liquidity.

- For Pharma, these structures can be tailored to the requirements and sensitivities of each partner, in many cases enabling what could be described as a P&L-sparing, “balance sheet supported” portfolio of innovative projects. This may not always be the interest of a partner, but accessing the otherwise inaccessible cash on the balance sheets of Big Pharma is a definite positive for these deal structures.

- For shareholders, including investors and team members, this model secures potential routes to liquidity that accrue as programs are progressed and monetized through development – importantly without having to sell the entire company. In essence this model creates the evergreen drug discovery stage biotech – a real unicorn in the history of biotech (because most drug discovery biotechs have to either sell or become later stage development players to achieve liquidity).

- Lastly, the structure has enormous financing flexibility: any individual subsidiary/program can be financed separately if desired – creating options for going longer on specific programs without diluting the parent platform company (or for a new investor, without having to fund drug discovery if that’s not their interest).

Nimbus certainly anticipates doing more of these types of structured transactions, both for its lead programs (IRAK4, ACC, Tyk2) and de novo collaborations around jointly-identified targets. Several of our other platform-based drug discovery companies, like RaNA Therapeutics, are structured in this way and will likely be pursuing deals of this type. Other drug discovery platform biotechs, like Forma and Viamet, have also been experimenting with versions of this LLC-holding company model. Several subsidiary-level deals have been done across the industry (like Forma-Genentech, among others). To my knowledge, none of these have yet to hit their acquisition-triggering milestones. It will be exciting to see what happens when this crop of deals matures to their pre-defined endpoints.

Creatively thinking about new approaches, new business models is part of innovating around the venture model – some experiments will work, some won’t. But the Nimbus experiment feels pretty good right now.