The biotech IPO market continues to march forward, with five new offerings expected to price in the next week or so. Investor demand for stories advancing novel innovative therapies remains at historic levels – extending what is now over a six-year window for biotech IPOs.

To frame up how the IPO markets have evolved over the past six years, it’s worth reviewing the data around the changes to pre-money valuations over time. The trend line is clear: up and to the right.

At least two observations from these data are worth noting.

First, the median pre-money valuation of new biotech offerings has risen in value from $150M to nearly $350M during this period – or an increase of over 130% from 2012-2014 levels. That’s staggering, and reflects the significant uptick in IPO demand, especially in 2017 and 2018, as this cycle has progressed. As the window opened in 2012-2013, things got exciting – but it’s twice as exciting now. In addition, from the downward valuation trend in 2014, its evident there was a mad rush to the markets that year of somewhat weaker stories on average – in line with 2014 being the biggest biotech IPO year ever. Fear of the IPO financing window closing was presumably a driver, too, in 2014 as historically windows were short (weeks and quarters, not years). But, as is usually the case, quantity is rarely a friend to quality.

Second, while the top quartile valuation range has largely been flat for the past 4 years (~1% change from 2014-2018), there’s been a huge increase in the bottom quartile: nearly a 150% increase in the valuation of the bottom quartile offering, reaching a $275M pre-money in 2018. The spread between the bottom and the top has contracted significantly: in 2015, there was more than a 4-fold difference in value from the 25th to 75th percentiles, while today that has reduced to less than 2-fold. This trend could reflect that the quality of the more recent IPO cohorts has increased dramatically, eliminating the less attractive offerings of the past that drag down the data distributions. Or it reflects that a rising tide is lifting all the boats, with greatest impact on the weaker stories floating in shallow valuation water. Only time will tell.

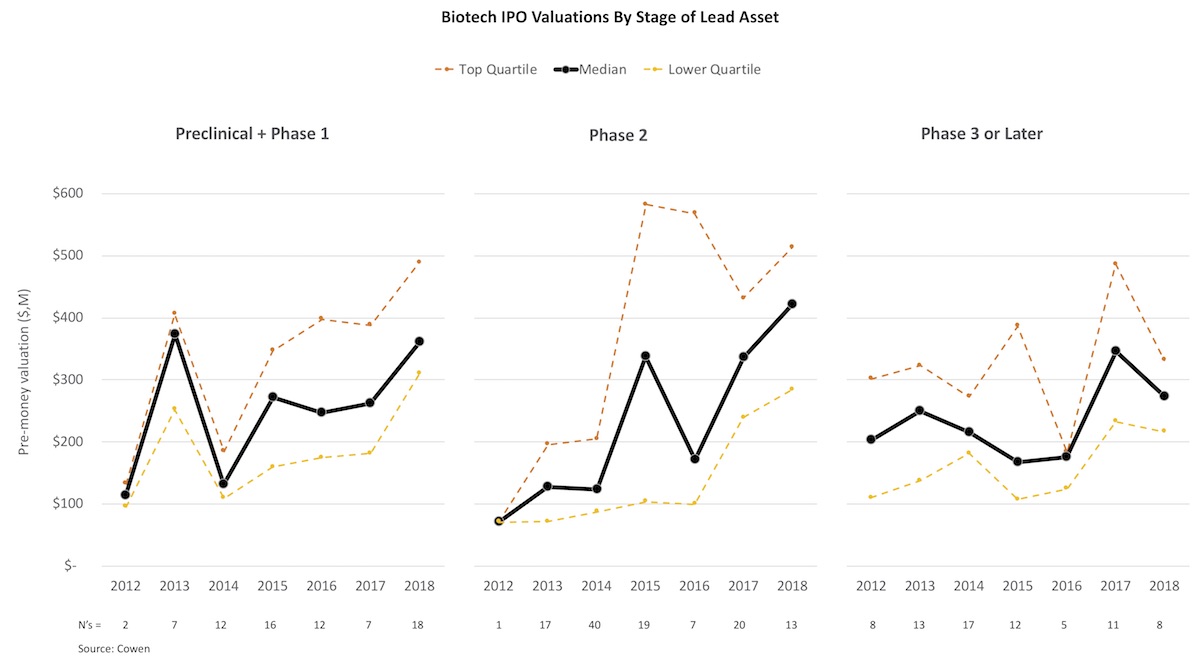

To explore the recent IPO trends further, it’s worth evaluating the maturity of biotech offerings over this period – by tracking the stage of the lead asset in R&D. (Thanks to data from the banking teams at Cowen, Wedbush, and BMO).

Preclinical and Phase 1 offerings have been far more prevalent in the past few years than earlier, representing nearly half of the offerings in 2018 to date (similar to 2016). In addition, the distribution of valuations has reflected the overall upward trends: 75% of this year’s early stage offerings have secured pre-money valuations above $300M, and 25% are above $500M. We’ve seen several preclinical offerings in recent years above $1B valuations – very heady prices indeed. These stories will obviously need to deliver on their bold promises to grow into those valuations.

Phase 2-stage IPOs haven’t been that different to their early stage counterparts: $300-500M represents the middle 50% of offering valuations, with tails above and below that range. The huge spread from 2015, perhaps reflecting the widely variant programs that “Phase 2” labels have historically been attached to, has also contracted dramatically.

Surprisingly, valuations of IPOs with Phase 3 or approved assets are the most muted in the group – no discernible trend across the past six years, with minor ups and downs along the way. Median valuations in 2012-2013 are only slightly below where they are today. Further, offerings of this stage have fallen from 75% of IPOs in 2012 to less than 25% today. Investors almost appear bored with these types of later stage stories, perhaps reflecting the reality that if these players had great late stage assets Pharma would almost certainly have tried to buy them.

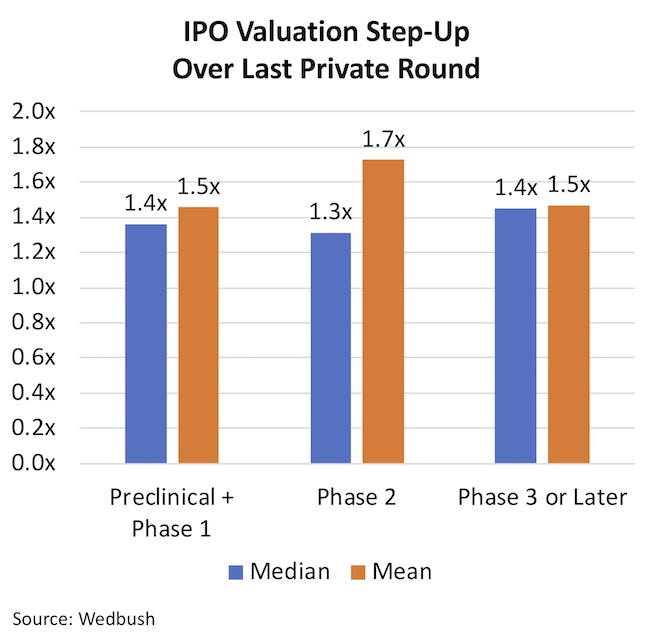

It’s not just that the public investors are buying into early stage IPOs with greater enthusiasm than later stage stories. As data from Wedbush shows, the mean and median step-up in valuation from the last private round to the IPO has been roughly the same regardless of stage (1.4-1.5x). This means that to support the valuation trends shown here, the later stage private rounds (aka “crossover” rounds) must be getting done at consistently robust valuations as well, and largely tracking with these trendlines. This is, of course, in line with the huge influx of venture funding into biotech over the past couple years (described here).

These data reflect investment community’s excitement about buying into bonafide therapeutic innovation: new modalities unlocking potential cures, new products based on transformational biology, platforms that can produce multiple first- or best-in-class programs – all with an expectation of these new medicines having a significant impact on patients. And with the prospects of learning/confirming the level of that impact in early stage clinical trials: the small “n” but highly compelling efficacy results that can drive enormous upside.

The current IPO backlog suggests the last quarter of 2018 will be very active, charting a course through several high profile scientific conferences (e.g., AASLD, ASH). As of now, public equity investor demand continues to show strength, which bodes well for a continuation of this IPO window and the aforementioned trends for high quality emerging biotech stories.