There’s “just too many early stage companies going public”, or so goes one of the most common lamentations about the current state of the biotech market.

I’ve read a good deal of venting covering this theme, including comments about VCs pushing low quality junk into the market, or others saying insiders should be locked up until a biotech’s first drug gets approved by the FDA. Much of this venting misses the mark, and in my opinion throws the baby out with the bathwater.

An open and permissive IPO market, and the flow of capital that enables it, has been a huge positive for the sector and for advancing innovation, and is not what caused the current market pullback.

As discussed in an earlier blogpost, a significant driver of the malaise in the markets has been the overall risk-off sentiment favoring value over growth, driving stocks in the innovation sector downward since Feb 2021, in particular as generalist funds moved elsewhere.

With that backdrop, there are, of course, a number of biotech-related issues, including the declining ratio of positive-to-negative newsflow in the sector as a whole, especially for clinical and FDA/regulatory events. Our sector’s woes been exacerbated by a lack of M&A by larger players in the ecosystem, which normally recycles capital, talent, and ideas.

But overall, I think it’s a mistake to blame “too many early stage IPOs” for the plight of the markets today.

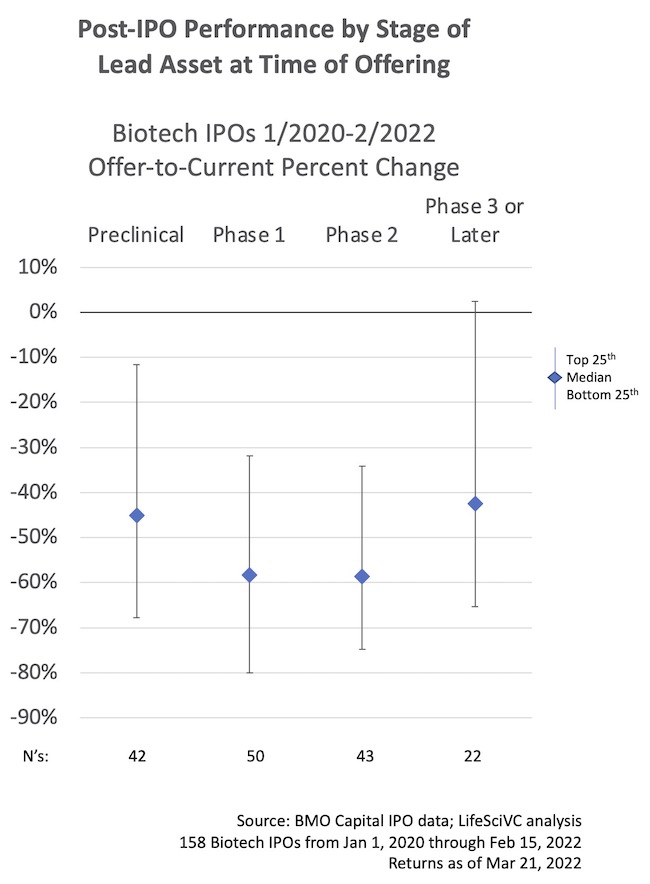

First let’s start with a little data, courtesy of the monthly IPO dataset from BMO Capital. Looking at 157 therapeutic biotech IPOs that went public in 2020 thru early January 2022, if you bucket them by stage of lead asset, there were 27% preclinical, 32% in Phase 1, 27% in Phase 2, and 14% Phase 3 or later. The after-market performance is captured in the chart below, as of March 21, 2022, with medians and quartiles. As is evident, the returns (losses) of these four groups of IPOs don’t track with stage. If it was true that the preclinical IPOs, the earliest of early stage, were the bigger cause of this market’s issues, you wouldn’t see this – you’d see a trendline towards “better” relative returns in later stage assets. That’s not really been the case.

While all these returns are horrible (and they are), they aren’t that far out of line with the rest of the market: the overall biotech market ($XBI) has delivered -47% since peaking in Feb 2021, while the average returns of this group are -37% from their IPOs in 2020-2022. Further, these data provide a counterpoint to the concept that early stage, preclinical IPOs are the culprit for dragging down the overall market. This also reinforces that IPO quality (caveat: if 1-2 year returns are actually proxy for quality) isn’t necessarily stage-dependent, but integrates a number of other factors related the science, team, and potential impact.

Given the debate about “too many” early biotech IPOs, I do think it’s worth reflecting more generally on the state of the biotech IPO markets and how we see the process as venture creation company-builders – so here’s a small treatise on the subject.

Stepping back for context, the biotech IPO market really began changing in late 2012, aided by the JOBS Act. We’re coming up on the 10-year anniversary of its signing on April 5, 2012 by President Obama. I’ve covered the IPO evolution in this blog before; in short, the “new” IPO process facilitated more fluid price discovery for private companies, whose end result was essentially an ever-open window, transforming the biotech sector from punctuated feast-or-famine cyclicality to a continuous conveyor-belt of access to scalable capital.

Today there isn’t a bright red line demarking “public” vs “private” biotech. It’s just a transition point from a relatively small capital pool (think puddle) to a larger capital pool (think ocean), with a commensurate increase in the number of shareholders. The “equity capital markets” start from when we do a seed round and continue through follow-on public equity financings done before a company hits profitability many years later. Different investors specialize at different phases, but for a company it’s not some sudden metamorphosis of a private caterpillar into a public butterfly. Instead, it’s a continuum of progression. The crossover phenom that emerged in 2012-2013 and accelerated recently has been a big driver of erasing whatever bright line there may have been between pre- and post-IPO biotechs in prior eras.

At Atlas, we start companies around what we believe is great science, finance them privately, take them public to access more capital from a broader set of investors, and continue to advance their pipelines and mature their platforms. Sometimes drugs emerge quickly, and sometimes it takes longer, with pivots along the way, with IPO and M&A events as a part of those journeys. Sometimes failure happens, and we try to find value out of the ashes (via reverse mergers, for instance). But bringing drugs to patients is the ultimate goal and long-term correlate for value creation – and it’s financed by all the phases of this capital market continuum from seed round to public follow-on financing.

To dive more deeply, here are seven observations around topics that are often misunderstood (or forgotten) about biotech IPOs today.

Caveat emptor. If you don’t like it when early stage biotech companies access public equity capital, then don’t participate in the offering. No one is ever forced to buy an IPO, and we generally don’t allocate much of the book to retail investors or fair-weather flaky funds. When I hear folks complaining about IPOs being “too early”, I just think about that fundamental rule of investing: caveat emptor. The buyer takes the risk. If you don’t want to buy into new offerings, you don’t have to. Rather than complaining that you got burned, don’t buy them. We generally participate in all of our portfolio’s private rounds and initial public offerings, as do most venture firms. The market for biotech IPOs over the past few years has only included willing participants, who were comfortable with the risk-return profile of the offering when they participated.

Drug timelines and risks aren’t linear with “R&D stage”. A frequent criticism of preclinical IPOs is that they are too far from the market and too risky. The reality is an Alzheimer’s project initiating a Phase 2a is likely farther from the market, and more risky, than many preclinical orphan disease plays (e.g., Agios and Blueprint took orphan cancer drugs from preclinical to registration in ~4 years). Serial entrepreneur Mike Gilman made a similar reflection in a pair of outstanding blogs on risk: arguing, for instance, an early stage oligo for SMA may be far less risky, and faster to market, than a mid-clinic rheumatoid arthritis drug (here, here). Understanding the nuances between different development paths with regard to risk, cost, and time helps underscore why generalizations are often wrong about preclinical or early stage stories.

Being public is hard, especially as an early stage company. Advancing a preclinical or early clinical company under the bright lights of the public markets isn’t easy. Public investors aren’t very patient at times, and every day volatility in the markets is a gut-wrenching rollercoaster. Many public investors also aren’t long term investor-builders; they’re traders looking to make quick returns, not to help make a drug. Working on the conversion of platforms into products in the public markets is challenging, and we know that going into the IPO process. The cold light of disclosure in the markets for preclinical companies means that important animal studies are material releases; that’s a tough place to be when you are working out the kinks, given how nasty the public market reactions can be. It’s also expensive to be public, with fees to lawyers and auditors, bigger finance and compliance teams, etc. And then there’s the “relevancy challenge” I’ve talked about before – staying top of mind for the 40 or so key institutional investors. So for those critical of “too many IPOs” I can assure you that no credible management team or Board thinks, “let’s go public because it will be fun and easy” – it’s not.

Instead, companies fundamentally go public to access bigger institutional pools of capital that aren’t available to private startups. If you want to scale your business, you need to access that bigger pool of capital. Over the course of biotech history, many great companies accessed the public markets as preclinical stories in order to raise more capital: Gilead and Regeneron in the early 1990s, Alnylam in early 2000s, and Agios, Blueprint, Intellia, Crisper in 2013-2016, to name only a few.

Anyone who has raised private rounds knows that the fundraising process is an arduous months-long proctology exam that ends in the issuance of senior preferred securities with special rights and privileges, including both debt-like and equity features, which is very different from the typical and straightforward common stock in public offerings. By going public, a biotech can access these larger and “cleaner” equity markets, which are essential to building and scaling R&D-intensive businesses over time.

Building biotech’s is a long-term journey, and having public investors as partners is therefore critical. Venture creation firms, as well as later stage VCs who focus on the midgame of emerging private investing, are important early in the life of a company, but don’t have the capital or decadal timeframes to advance R&D from discovery idea through to the market all by ourselves. We need public investors as partners to continue this journey together, and many of these players participate with us by crossing over into pre-IPO private rounds – enabling a smooth transition into the public markets. Thankfully, there are enough deep-pocketed, long-term public equity specialists in our field to work with us as we build and grow these biotech firms. Sure, having the big long-only “generalist” funds engaged in biotech is important in the long-run, and they’ve been out recently with the “risk-off” environment, but the reality is they have sat on their hands at prior pullbacks in the market too. And day-trader retail investors, who may be helpful for day-to-day liquidity, are not really the deep-pocketed company-building partners a biotech needs in the long run. It’s worth nothing that any VCs who constantly throw junk at these important downstream public equity partners aren’t likely to be in the business over multiple cycles.

An IPO isn’t an exit, it’s a financing. Despite the oft-cited myth that VCs dump at IPO or after the lock-up expires, the reality is we (and most VCs) are in our companies for years following an initial public financing. The lock-up of private shares into an IPO is part of what prevents the immediate “dumping” of shares, but, more importantly, in many cases our investment thesis hasn’t played out yet and we remain focused on delivering that aim – that’s where big value inflections occur. We’re often still on the Board and actively involved in strategy and governance in these newly public companies, and thus are limited as insiders to certain windows given material non-public information. Like most insiders, we generally put in place 10b5 plans to programmatically exit a position in small quarterly increments over multiple years. This hurts our returns when stocks run upward over time, and helps them when stocks later go down – but we never know that in advance, just like an executive’s 10b5 stock plan. We also often hold a significant “tail” portion of a position well-beyond that time in the hopes of an outlier $10B+ outcome. Follow-on financings in the 1-2 years after an IPO are also just financings thru a primary issuance of stock – to raise money for the company; it’s very, very rare to see a secondary “sale” of a private holders’ shares into a follow-on equity financing. In sum, IPOs aren’t exits for VCs at all – they are just financing points on the long arc of building biotech companies. And given the limited daily trading of newly-minted public companies, an IPO isn’t real liquidity for any significant existing shareholders; it’s a step along the path to progressively increasing liquidity over multiple years.

Going public also has some material drawbacks for private investors. Upon going public, private investors lose their downside protection and special rights, thru the conversion of preferred stock into common shares. This includes forfeiting preferred liquidation rights (in case the business is sold or shutdown) and governance rights (e.g., vetos on certain corporate decisions, special voting thresholds, etc). These liquidation stacks can meaningfully alter the return profile in favor of investors over other shareholders. The loss of these rights greatly diminishes the legal and financial protections and privileges of existing private investors (like VCs) in the process of going public. Further, private shareholders take on significant dilution by going public. That dilution not only comes from the sale of new stock in the IPO itslef, often in the 20-35% range, depending on valuation – but also from “evergreen” stock option plans approved at IPO. These evergreen programs add 4-5% dilution annually, to incentivize executives and the broader team, which adds up to 15-20% dilution after 3-4 years. That’s like a “full” follow-on offering of dilution done in a silent way. We can argue about the merits of this, but today it’s a mainstream part of the compensation model found in almost every IPO. These two elements (i.e., the removal of the preferred stock overhang and more stock via the evergreens) are both subtle incentives for management teams to want to go public, and both are generally not beneficial for private investors. But it’s all part of the tradeoff of accessing bigger pools of capital to scale companies, and one most VCs support in the right context.

Private and public investors, and management teams, make and lose money post-IPO. Sure, did some new investors get burned by buying newly-minted IPOs, or management teams lose out by getting now underwater options as compensation? Yes. Welcome to the way capital markets work. We’ve made and lost money on our investments in the public markets. I’ve been around long enough in the sector to see the ups and downs of the public markets many times, and have been burnt many times along the way. While there are obviously some examples of over-promotional “pump and dump” schemes, leaving public investors as bag holders, this isn’t a widespread phenomenon across the sector, especially amongst quality institutional investors. Maybe I’m too idealistic, but I sincerely believe most of the practitioners in the private biotech space (management teams and VCs) actually believe in the potential value of the drugs they are advancing – whose value will accrue with longer term patient impact.

These observations aim to shed light on how early stage investors and biotech management teams typically think about the biotech IPO dynamic.

Before concluding, it’s worth raising a few concerns around the current biotech IPO markets, related in some way to the concept of “market indigestion” from the prolific IPO environment of the past few years. Since 2019, we’ve added over 200 public biotech companies, both early and later stage, and that’s a lot for the markets to digest.

The big question is whether there really were “too many” IPOs? Easy to Monday morning quarterback about how the game was played, harder to do beforehand. Prospectively, my guess is, like the Lake Wobegon Effect, every management team and investor behind the IPOs of 2020 and 2021 thought they were an above-average story. They had bankers, lawyers, auditors all telling them they were ready. They had strong enough Test-the-Waters meetings with public investors to support going public. They did price discovery around valuation in that process and picked a range that matched investor demand. And most of them raised the amount of capital they hoped for, and a surprisingly high percentage were priced in or above the range (suggesting the valuations met market demand). That’s the way the markets work, but only in hindsight does it become clear which companies were successful, and what number of IPOs was the “right” number. There isn’t a fixed “right number” of IPOs in a given a year. Were 10 IPOs annually in 2010-2011 too few? Was ~90 in 2021 too many? If there were more Pharma M&A recycling capital, should the IPO number be higher? Only the market really knows – it integrates past feedback and self-adjusts around the quality of the IPOs that come to market. If the market feels there were too many, or quality was too low, or the overall sentiment is too challenging, then the bar will go up – and it’s pretty high right now.

One legitimate concern about the number of IPOs in recent years is that many of these will need to finance again, and within the next few years. This is a big difference with most tech IPOs: newly public tech companies are often profitable, or could be if they needed to be. With biotech, essentially none of the recent IPOs are anywhere near profitability, and that means they will need to tap the follow-on equity markets every 1-3 years to fund their R&D programs. Morgan Stanley just estimated that ~30% of public biotechs they follow (~400) will need to finance this year, in line with historic averages in terms of numbers of companies needing to fundraise, but likely 3-fold higher in terms of aggregate capital needs due to burn rates. If the markets remain in a risk-off sentiment, there will be biotechs who could run out of fuel – either forced to do less favorable deals with pharma, or go down path of firesale M&A, delisting, or even bankruptcy. Given the amount of capital on the sidelines, higher quality names will be able to finance, even in this market; as an example, the upsized follow-on financings of Apellis and Argenx last week. But more speculative names could struggle to catalyze interest. Allocation of capital is a big part of the role of the market, and every smart company is thinking about managing their burn rate differently today (vs in Feb 2021).

Another concern is that of hyper-competition, and how the permissive IPO market may be making this issue more challenging to manage as a sector. It comes down to the question of whether there are too many public (and private) companies chasing the same targets and same indications. This is a perennial problem in the biopharma industry, and one I’ve covered in the past, describing the march of the lemmings in cancer or the supernova in immune-oncology, for instance. It’s normal in our industry for Pharma R&D groups and biotech firms to all chase the hot new targets with slightly different versions of “novel” therapeutics: through competition, better products emerge for patients. Interestingly, the same thing happens in the tech markets, where abundant capital and excitement around “hot spaces” (targets) creates dozens of food delivery or ride hailing firms, as examples, and only a few survive.

But this is a broader question than public vs private, and whether we’ve had too many biotech IPOs: it’s a question about how to deal with the fallout of competition. Historically, the shake-out for winners vs losers would come largely in the pruning of pipelines of large Pharma and a few public and private biotechs. Today we’ve got hundreds of recently public SMID-cap publics also involved in this product differentiation shake-out, without unlimited access to cash to deliver on their theses. And they can’t quietly prune programs as a private company anymore. This hyper-competitive dynamic is likely to be painful for the “losers” that lack differentiated assets in some of the over-heated, over-invested areas, and public investors need to brace for that outcome. Picking winners will be even more important.

Even with hyper-competitive markets, and the increasing need for public follow-on capital, I would strongly argue an open and prolific IPO process is a good thing for our industry, and for innovation. The market will tell us real-time how many early stage IPOs it wants to digest – I’m hopeful its appetite remains healthy and robust.

Especially because I remember when the IPO market wasn’t healthy – in fact, it was broken.

After the poorly performing IPO market of 2005-8, and then the financial crisis of 2008-9, it was clear the biotech IPO model wasn’t working. I wrote a piece in Nature Biotech called “Beyond the Biotech IPO” – saying the IPO process was busted and we need to fundamentally change the business model, incorporating elements like equity capital efficiency, leaner and more distributed operating models, greater reliance on innovation (vs spec pharm), and more active partnering with Pharma.

A few years later, without any real improvement in the IPO markets, BioCentury published a Jan 2012 editorial written by Stelios Papadopoulos, John Maragonore, and Moncef Sloui, titled “Pharma To Support Biotech IPOs”. It essentially said that the biotech IPO model was indeed busted, but that without a viable IPO market the future of biotech was at stake: companies can’t advance new drugs without capital. They further argued that Pharma depended on biotech, and therefore should pool its resources to create a biotech IPO support fund, of sorts. Thinking about that editorial, and the dismal market climate back then, is a great reminder of how incredibly dire things were for creating and building biotechs without a functional IPO process.

After a 10-year open window for IPOs, including early stage stories, and an incredible era for innovation funded by the equity capital markets, we need to make sure in our visceral response to the challenges of the current IPO markets we don’t throw the baby out with the bathwater.